How our people, technology and capital make us different

Learn about how our people, technology and the way we manage capital makes us different.

When people first learn about what we’re doing at vabble one of the first questions we get is: how do we address issues with cost of capital and price our products competitively across the region?

Although there is an implied cost of capital with our work, it is by definition lower than most other financing activities. At vabble, we don’t lend money. Instead, we are buying an asset on behalf of institutional investors (i.e. pension and insurance funds). These institutional investors allow us to offer our workflow automation with an implied low cost of capital and in turn pass that benefit on to the users of the platform.

This is a key part of what makes us different from other financing options for exporters across emerging markets – be that Latin America, Africa, or Asia. We don’t have a standard loan pricing business model and we are not bound by typical banking concepts, which is why it’s beneficial to understand how our business model works and where our competitive advantage lies.

In this article we’ll make it clear exactly how vabble addresses cost of capital by covering the following:

- What’s our competitive advantage as a company?

- Capital: we’re not a lending business, we’re connecting investors to assets and offering exporters access

- Technology: exporters and investors are two sides of the same coin, and can do it all online, from one platform

- People: we’ve got all the right connections in the right place, people and technology

- How vabble makes money

Note: vabble is currently raising investment. To learn more about how to invest in vabble, contact investors@vabble.io .

What is vabble’s competitive advantage?

We often get asked: what makes you stand out, and how do you know someone can’t come in and copy what we’re doing?

In other words, what is our moat ? Our sustainable competitive advantage?

vabble’s moat is a combination of elements that other companies just aren’t able to put together as they are bound to other business models. Those elements are: our access to institutional investors, our technology and our team, on and off the ground.

To learn more about our story, head to: Exporters need financing and institutional investors need good investments. Here’s how we’re connecting the two.

Let’s dig into three key aspects of our competitive advantage:

- Capital

- Technology

- People

Capital: we’re not a lending business, we’re connecting investors to assets and offering exporters access

vabble’s focus is on monetising assets, creating liquidity, and lowering debt, particularly in emerging markets with limited access to capital, while also offering institutional investors an opportunity to invest in a completely new (untapped) market that for Latin America and Caribbean alone stands at $655 Billion of payment flow from UK, EU, and US. Our approach is to monetise these cross-border export receivables payable by UK, EU, and US buyers.

Unlike many lending businesses that focus on emerging markets, our model does not rely on finding borrowers to pay high-yield rates. Instead, we focus on allowing institutional investors to buy high quality receivables (while offering liquidity and helping the exporters) and therefore get a higher return than on comparable assets. With this approach, no one becomes a borrower: the exporter is simply getting the payment they’re due, earlier, with a small discount to account for the time value of money, and vabble’s workflow automation.

With vabble, there is no direct cost of capital comparison because alternative capital is typically in the form of debt, and of limited availability. Instead, when an institutional investor purchases a receivable, they are providing liquidity from their cost of capital, and a required return. Since we’re dealing with high quality assets and institutional investors, our implied cost of capital for providing liquidity turns out to be incredibly competitive.

It’s important to note that we unfortunately can’t work with just any exporter: we’re working with exporters that have receivables from well known European and American companies, that can also be backed by trade credit insurance.

That’s why it’s as if investors are investing in receivables from companies in Europe or the USA – the only aspect that’s different about them is their location: exporters are based in emerging markets as opposed to a supplier in say, Dusseldorf. That’s how we can make available a high quality receivable for a good price to the investor, as well as liquidity at a good price to the exporter. Insurers also welcome this additional business with open arms, as is executed with high visibility and full transparency.

To make this clearer: think about the price of a bottle of water in the supermarket (where you might pay 95p) and compare with the price of a bottle in an airport (where you might pay £4). As property investors say: location, location, location. The quality of the product is no different, but the price is largely a factor of where you’re buying it.

There is a flip side to this dynamic at play with the assets vabble enables institutional investors access to. We’ve found a great interest in exporters offering in emerging markets, and we are starting with Latin America.

After cash, the most liquid asset for an exporter is a good receivable – but exporters in emerging markets have few options to turn those receivables into cash. Before vabble, they would have had few private credit options, in local currency and at very high rates of interest. Any of these alternatives are very restrictive, often asking for personal guarantees if available at all. This is why there’s an estimated SMB trade finance gap in Latin America of at least $350B .

For the exporters we work with, vabble can provide them with the cheapest marginal additional unit of capital they will be able to secure. Simple, smart, and always on. As long as they do business with high quality companies, the exporter can continue to have access to this source of financing.

It works wonders because the exporter does not become a debtor. There is no loan, which means there is no additional debt in the user balance sheet, and the convenience of accessing cash immediately makes vabble a perfect tool to become a key part of the exporter working capital stack.

All the costs associated with selling the asset are reflected in the discounted price of the receivable. vabble fronts the purchase while the asset is effectively sold back to back and bought by an institutional investor. The convenience of accessing capital on the platform, soon after the exporter invoices and ships, without going to any bank and without taking on debt, makes vabble the perfect addition to the working capital stack of companies in emerging markets.

For the companies and receivables that qualify, vabble is the simplest and smartest most competitive additional unit of capital.

vabble’s main goal is enabling faster payments through helping exporters turn quality assets into liquidity. Now come into play the other two elements of our competitive advantage: our technology and people.

Technology: exporters and investors are two sides of the same coin, and can do it all online, from one platform

The idea behind vabble is: let’s connect institutional investors to emerging market exporters with high quality receivables through a neobank-like platform.

The technology allows investors to seamlessly enact every step of investing in the trade finance asset class using workflow automation, and that same automation enables exporters to access liquidity by selling their quality receivables. This is one of the reasons our platform stands out in the market, along with full transparency and the absence of balance sheet risk.

We’ve invested a significantly into making vabble a unique source of truth neobank-like platform, allowing exporters to upload invoices and get funding with just a few clicks or finger taps. Through the use of Tradeteq, institutional investors can easily get access to those invoices.

To make trade receivables investable, it’s vital that the legal framework is reliable, to allow trade receivables to be sold on a “true sale” basis. vabble has retained the counsel of Sullivan & Cromwell, who developed the global standard for receivables purchase agreement.

With exporters in emerging markets and investors in developed markets using the same framework agreement, vabble can offer convenience to exporters as it is a well known, tried and tested type of agreement. To top it off, there’s no need to deal with a bank: just upload information about the receivable to the platform, and vabble checks:

- The buyer, or obligor, confirming the invoice

- It can be trade credit insured

- It’s not fraudulent

Then, cash is paid to the exporter’s account of choice by vabble’s bank, JP Morgan. At this point, vabble does not offer FX or hedging capabilities, but these are on the product offering roadmap.

At vabble, we’re not a bank and we are not a financier. We know finance, but we’re a technology company. And that unit of capital – what vabble is offering to the exporter – is not debt, but liquidity. This means:

- There are no adverse selection issues: since we’re not a bank, we don’t have conflicts of interest with other financing activities.

- We can respond to the requirements of institutional investors and present them with opportunities. For example, we know the institutional investors mandate is investing in assets rather than companies, and want full transparency and visibility.

- We’re offering investors the flexibility to pick the assets they want, in the same way you can choose your dishes from the conveyor belt in a sushi restaurant.

- Exporters can manage their working capital without becoming debtors, therefore getting cash faster without increasing liabilities.

Two other key parts of our technology are our partners:

- Tradeteq, which connects with institutional investors

- JP Morgan, which enables payments, collections and reconciliation

Tradeteq is a trusted third party that is a key part of the vabble infrastructure, allowing institutional investors to commit capital and look for and monitor and report on the assets they invest in. Tradeteq provides regulated entity services and acts as a third party program manager that earned the trust of the investors. It provides real time NAV calculations and takes care of the reporting, regulatory and data residency requirements while offering a clear view of the investor portfolio.

JP Morgan, on the other hand, manages segregated funds for the investors without commingling and takes care of all the payments, with great coverage in Latam and worldwide. We’re integrating the JP Morgan payment system into vabble, to enable payments, collections, and reconciliations directly within our platform.

But all of this is still replicable, if it weren’t for the last jigsaw piece of our competitive advantage: our people.

People: we’ve got all the right connections in the right place

Pablo Terpolilli founded vabble in 2021, with Derek Hudson joining the business as founding partner shortly after. Both are former bankers with vast experience in emerging markets, on both commercial and banking sides.

Between them, Pablo and Derek have 65 years of experience in banking and finance. Some of Pablo’s experience includes:

- 5½ years at Goldman Sachs running the private financing business of Latin America.

- 2 years at Standard Chartered running the Western Hemisphere private financing business.

- 3 years at UBS co-running the EMEA special situations financing group.

Pablo’s reputation and contacts have helped vabble attract the backing of some of the largest financial players in the world, with JP Morgan as the house bank and the main payment services provider, and Goldman Sachs and other institutional investors as investors in receivables.

The institutional investors working with vabble know Pablo, in many cases having worked with him for years previously. They trust his judgement and appreciate how transparent he is in his operations. They also know he understands emerging markets and the Latam region well, and can engage with both the exporters and their suppliers.

Beyond that, Derek’s deep and vast network and experience in the region helps the entire commercial, onboarding and KYB processes. Compliance with institutional investor standards of KYC, AML and sanctions checks are paramount at vabble, and carried to the highest standards.

The fact that Pablo and Derek know Latin America so well is exactly why vabble is starting out in Peru and Ecuador, before expanding to Brazil or Mexico. Not just that, but vabble attracts top talent globally, and has experienced bankers on the ground that know the trade and have prior relationships with many of the exporters, which were their clients while they worked at their respective institutions.

Pablo is from Argentina himself, and hand-picked every team member on the vabble team. His partner, Derek Hudson, is one of the best known people in the trade finance space, and was recently recognized by his peers at the Annual ITFA Conference in New York as one of the top five people to impact the trade finance industry over the last 30 to 40 years.

Derek and Pablo have known each other for over 25 years – when Pablo discussed the idea with him, Derek immediately understood it as a win-win business, and was ready to sign on. He’s worked for over 35 years in Latin America correspondent banking and trade finance activities, and started several Latin American lending departments from scratch. The last two banks he worked for reached over US$1 billion in exposure through the regions.

Colleen, one of vabble’s key operators, is a former portfolio manager at Schroders, and has run and operated two startups for the past 12 years. Pablo and Colleen met at a Babson Graduate gathering in London (the number one school for entrepreneurship in the world, of which both Colleen and Pablo are graduates), and she joined the vabble team because the company marries two things Colleen has a lot of experience in: finance and tech.

Then there is Francesco, a former McKinsey partner, and Simon, who has recently joined from Goldman Sachs Asset Management where he was a Managing Director, with primary responsibilty for technology development. The vabble team have backgrounds at Goldman Sachs, McKinsey, UBS, Merrill Lynch and so much more. The list goes on – everyone at vabble contributes in their own strategic way, and that brings a diversity of experience that makes them integral to the culture, and the mission.

How vabble makes money

So how do we make money?

Simplicity goes a long way. From the beginning, our objective is to have very simple pricing. We have not implemented a SaaS, subscription model, and we don’t include the day-to-day operation costs in our pricing. Those costs all come off our margin, so we have no hidden fees.

Our primary revenue source is a percentage cost plus a per-transaction spread, charged on top of the institutional investor's required return base cost. Exporter companies pay this fee through a discount to the receivables' face value. It is a usage based model, of a compelling proposition: getting invoices paid ahead of time. Even during the best of times that is a tall order.

Here’s an example of how this works in practice:

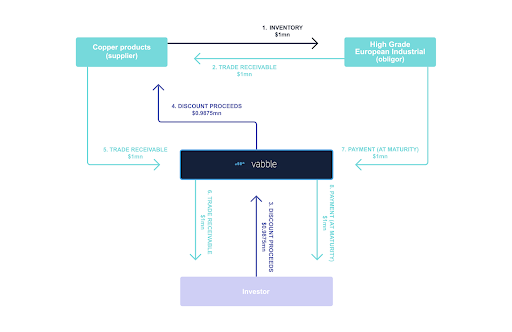

- vabble receives a good receivable of $1,000,000 that’s payable in 45 days.

- We buy that asset out of a special purpose vehicle (SPV) entity in Luxembourg.

- The institutional investor funding the vehicle states their requirements for the assets they want to buy, such as: a) High grade companies b) Insured c) Avoids certain merchandise like oil, firearms, tobacco d) Maintain certain concentration limits on seller and buyer sides e) Monitor any commercial disputes and non-payment events

- The institutional investor also states their required rate of return, and vabble adds a margin on top. Then, for the sake of the example, let’s say the implied discount rate is 10.5%. vabble purchases 100% of the receivable on behalf of the investor, and the payment terms are 80% of the invoice value upfront minus the implied interest cost($800,000 - $10,500 = $789,500), and 20% is deferred to the original payment date ($200,000).

- The exporter immediately gets $789,500, and receives the 20% that’s left when the invoice is paid by the buyer. Normally after the 45 days, plus or minus any adjustment to actual pay date

- The investor’s interest income is therefore at a rate of 10.5%, which for 45 days pro rata is equivalent to $10,500

- vabble aims to make a 2.5% per year gross margin equivalent in the internal purchase and resale of each receivable.

By purchasing receivables rather than using financing, this model gives exporters that use vabble an advantage over the exporters that use traditional financing methods: a win-win situation.

We’re also looking forward to offering more options and exploring additional revenue channels, such as compelling FX rates, and some other supportive services such as hedging, or other scheduling and automations around fast payments. For example, as we process data, we’ll be able to provide plenty of insights to our users based on usage patterns and uptakes.

Learn more about investing in vabble

In this article, we’ve explained vabble’s moat and how our capital, technology and people are what allow us to have a sustainable competitive advantage in the market. A market that remains “unseen” at $655 Billion payment flows per year, just to Latin America and the Caribbean, from buyers in the US, UK, and EU.

We're combining technology, a vision, and access to institutional investors, backed with many years of experience and knowledge of the valuable Latin American market, plus a network of contacts that trust and respect vabble’s co-founders Pablo and Derek and the team they’ve put together, breaking silos, connecting dots that were not previously connected..

All of this adds up to create a business model that is not easily replicable, and means we can offer a unique proposition: uncovering an untapped very large market to provide fast payments to exporters, advancing cash against quality receivables at a competitive price, and offering high quality assets to institutional investors.

To learn more about investing in vabble, contact investors@vabble.io .

5/17/2023 - vabble team -

4/3/2023 - vabble team - finance, vabble, investment